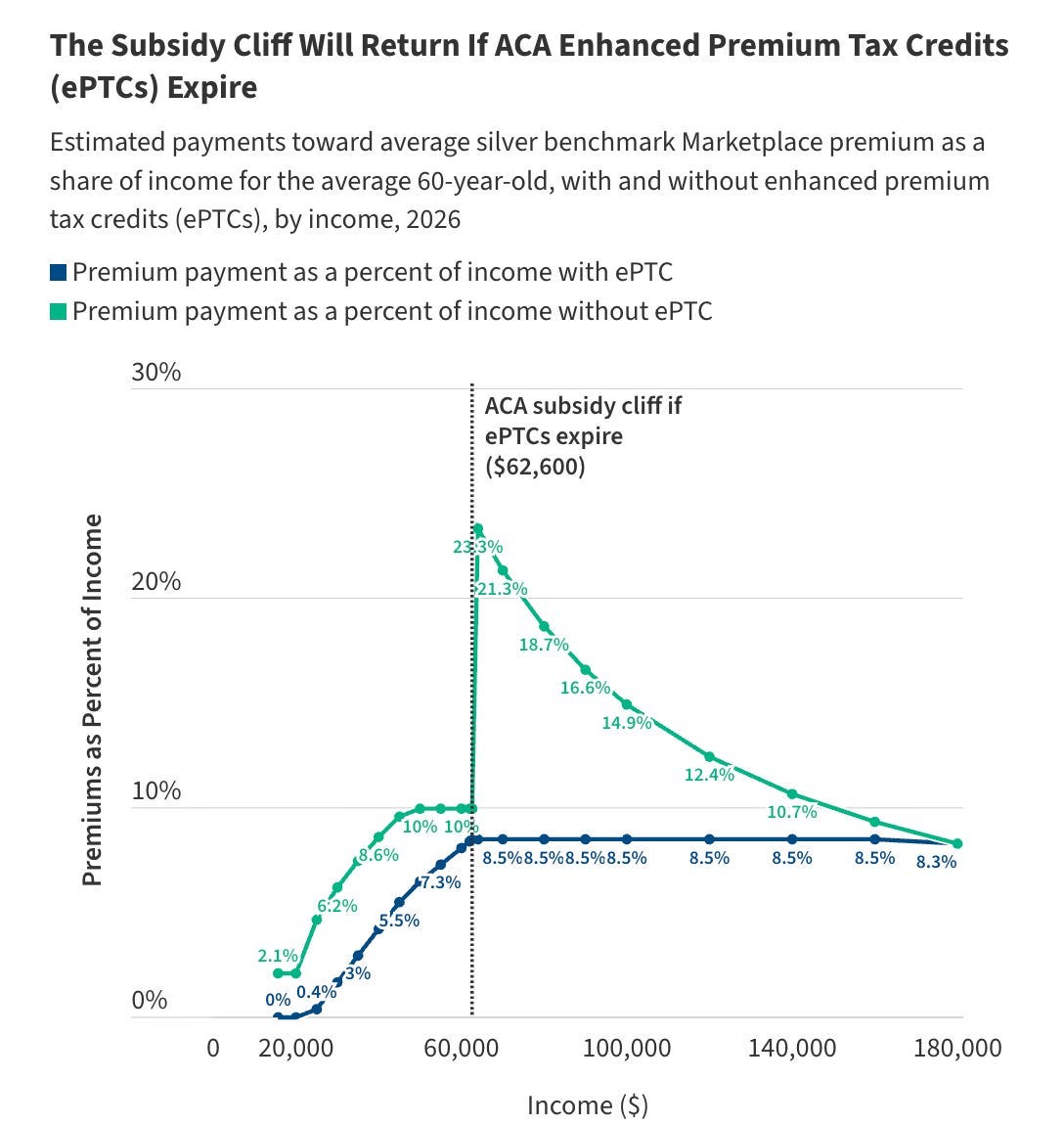

On December 31, 2025, enhanced Premium Tax Credits (ePTCs) officially expired, eliminating $0 health insurance premiums for low-income earners and restoring the subsidy cliff: as of January 1, 2026, anyone earning even $1 over 400% of the federal poverty line ($62,600 for individuals) is responsible for the full sticker price.

ePTCs were introduced by the American Rescue Plan Act of 2021 and extended by the Inflation Reduction Act (IRA) so that no one had to pay more than 8.5% of their income for the silver benchmark plan. As a result, Affordable Care Act (ACA) Marketplace enrollment grew from 12 million in 2021 to 24.3 million in 2025, while net premium costs fell by 44% on average. Ironically, the Republican states of Texas and Florida that fought hardest against the ACA were the largest beneficiaries of IRA subsidies, receiving $1.5 and $2.2 billion in 2024 respectively.

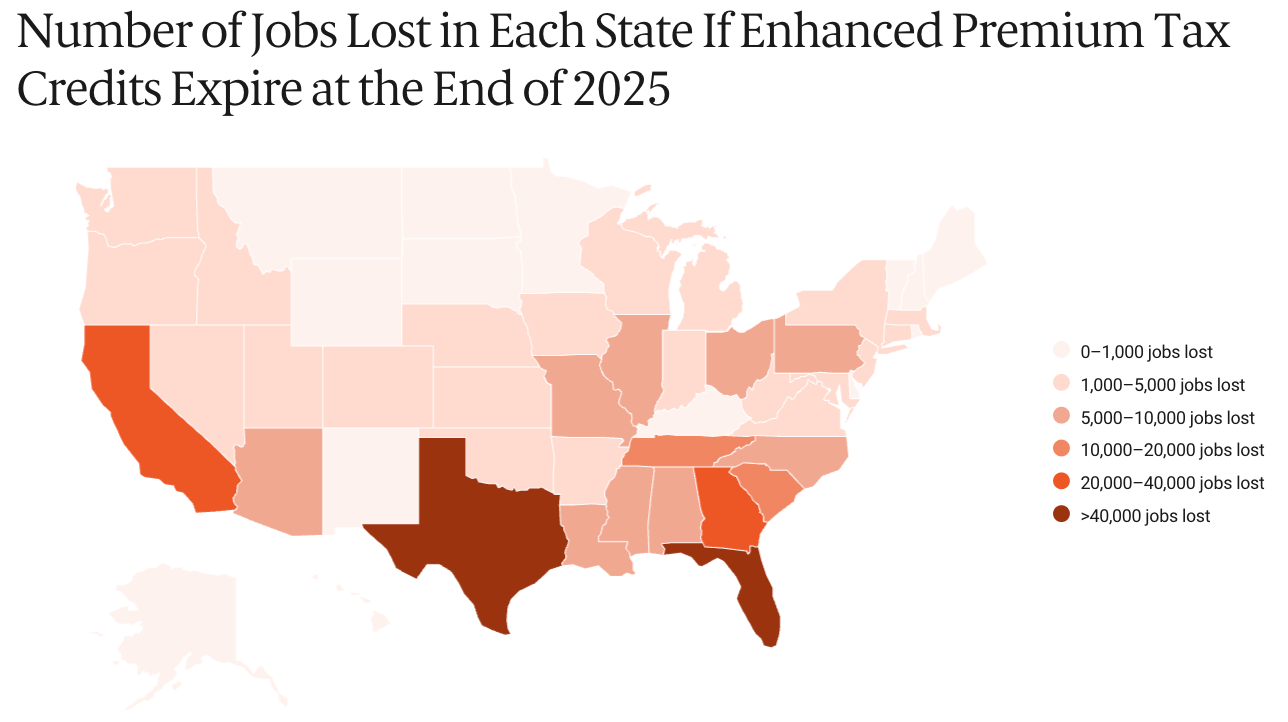

According to the Urban Institute, a nonpartisan think tank, the expiration of ePTCs will cause net premiums to roughly double for people earning over 250% of the poverty line and quadruple for those earning less. An estimated 4.8 million people will lose health insurance in 2026. Meanwhile, the Commonwealth Fund, a health policy group, projects a $40.7 billion drop in GDP and loss of 340,000 jobs, disproportionately affecting Texas and Florida.

On September 19, 2025, Senate Democrats took advantage of the 60-vote filibuster threshold to block H.R. 5371, demanding that any bill to fund the government include an extension of enhanced subsidies. Republicans refused to compromise, triggering a government shutdown beginning on October 1 that would become the longest in US history. However, when the 43-day duration began to disrupt federal food assistance programs and airport operations, eight moderate Democratic senators agreed to a short-term funding bill that crucially did not extend ePTCs.

The Republican Party opposed the extension on the grounds that it would increase the deficit by $350 billion over ten years, function as a subsidy for insurance company profits, and provide little patient value. On the other hand, the deficit cost would manifest itself in higher hospital bills for everyone else to cover the costs of emergency care for uninsured patients, while the ACA’s 80/20 Rule requires insurers to spend at least 80-85% of premiums on medical care. Furthermore, people who decide against purchasing health insurance are not doing so because they do not value it, but because they are priced out. The United States has the highest health care costs in the world, and coverage can quite literally be the difference between life and death.

In light of the expired ePTCs, the Trump administration has proposed a “Great Healthcare Plan” that seeks to lower health care costs. On February 3, the president signed H.R. 7148, which implemented part of the plan by removing perverse incentives for pharmacy benefit managers to drive up drug prices, requiring hospitals to use unique National Provider Identifiers (NPIs) for off-campus outpatient clinics to ensure site-neutral payments, and codifying most-favored-nation (MFN) deals so that the US pays the same prices as other developed nations for certain prescription drugs.

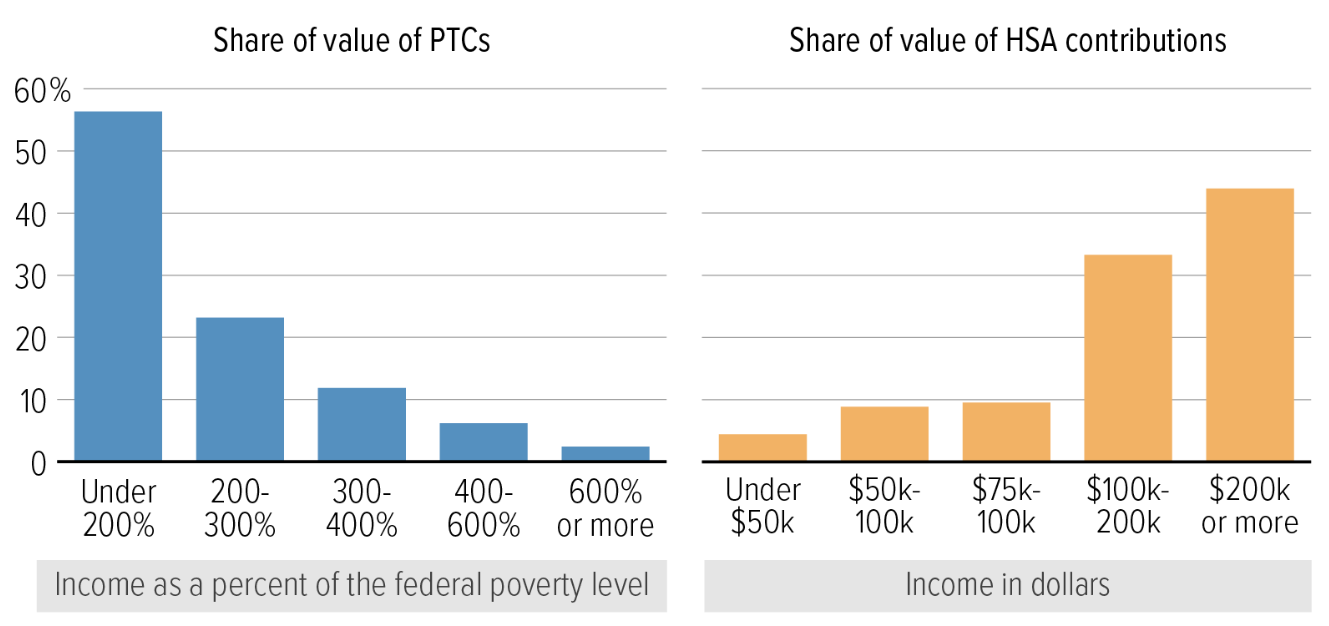

While these policies are a step in the right direction, the bigger question is what will replace the enhanced subsidies. Republican Senators Rick Scott and Bill Cassidy propose depositing the $350 billion earmarked for ePTCs directly into Health Savings Accounts (HSAs) that individuals can use to pay for health care. However, an HSA deposit of $1000-1500 would do little for people like Adrian Pitts, a 57-year-old small business owner and North Carolina resident who just saw his monthly premium rise from $1000 to $2670 and is now considering bankruptcy insurance. Meanwhile, HSAs will incentivize healthy people to choose cheaper Bronze plans, leaving a sicker, higher-risk population in the more comprehensive Silver and Gold tiers. This adverse selection threatens even higher premiums for those who need coverage the most.

Fundamentally, the debate over ePTCs and HSAs misses the forest for the trees. By treating health care as a commodity instead of a right, the United States is not saving money; it is merely shifting the cost. When millions like Adrian Pitts are priced out of preventative care, they inevitably return to the system via the emergency room, where we pay twelve times the cost of a doctor’s visit to stabilize crises that could have been avoided entirely.

| A guest post by

|